Could a latent defect from the 1990s suddenly jeopardise your current capital expenditure plans? With 88% of commercial sites estimated to be underinsured and the Building Safety Act retrospectively extending limitation periods to 30 years, the regulatory framework governing liability for structural failure in commercial property has fundamentally shifted. It’s a reality that places asset managers in a difficult position, as historical oversights now carry modern legal and financial consequences that traditional insurance policies may fail to cover.

You’re likely aware that the clarity once offered by “Full Repairing and Insuring” (FRI) lease obligations is eroding under the weight of new legislation and rising premiums. This article serves as an authoritative guide for asset controllers, detailing how to address complex liability through empirical engineering rigour rather than mere administrative compliance. We’ll analyse the impact of the Building Safety Regulator’s 2026/2027 fee structures, the necessity of the “golden thread” of digital information, and the role of advanced materials science, such as Tyfo® Fibrwrap® Systems, in extending the functional lifespan of critical infrastructure.

Key Takeaways

- Differentiate between latent defects and gradual deterioration to accurately assign financial responsibility amongst landlords and tenants in accordance with current legal frameworks.

- Navigate the stringent requirements of the Building Safety Act 2022, focusing on the expanded role of the Accountable Person and the 30-year retrospective limitation for claims.

- Mitigate the risk of underinsurance by addressing the inevitable deterioration that standard building policies exclude, ensuring comprehensive protection against liability for structural failure in commercial property.

- Assess the technical viability of structural life-extension through specialised interventions such as Tyfo® Fibrwrap® Systems, which provide a permanent alternative to costly and carbon-intensive demolition.

- Streamline remediation projects by appointing specialist contractors who oversee the entire lifecycle of the intervention, from initial structural surveys to the management of complex temporary works.

Defining Liability for Structural Failure in UK Commercial Real Estate

The allocation of legal responsibility for the structural integrity and failure of a commercial asset is rarely a binary matter. It involves a complex interplay between landlords, tenants, and management companies, often governed by the specific covenants of a lease or the technical history of the build. Within this framework, the primary challenge lies in the distinction between latent defects, which are inherent flaws in design or construction that remain hidden for years, and gradual deterioration, which results from the predictable wear and tear of building materials over time. Whilst the former may trigger claims against original contractors or insurers, the latter is frequently classified as a maintenance failure, placing the financial burden squarely on the party responsible for the building’s upkeep.

The concept of “fitness for purpose” adds another layer of complexity. In commercial real estate, a structure must be capable of supporting its intended operational loads without compromising safety. If a building’s load-bearing capacity is found to be insufficient for its designated use, the liability for structural failure in commercial property can escalate into a professional indemnity crisis for the engineers involved. It can also trigger public liability claims if the failure presents a risk to occupants or the general public. These risks are not merely theoretical; they represent significant financial exposures that require precise technical mitigation.

The Full Repairing and Insuring (FRI) Lease Framework

Under the standard FRI lease model, the obligation to maintain the building’s envelope and core structure is typically transferred from the landlord to the occupier. This shift creates a significant liability for structural failure in commercial property for the tenant, who becomes responsible for remediation costs regardless of the building’s age. Disputes often arise when “inherent defects” are identified, as tenants argue they shouldn’t be liable for flaws that existed prior to their tenure. To mitigate these risks, sophisticated asset managers utilise detailed Schedules of Condition. These documents serve as an empirical baseline, protecting occupiers from being held accountable for pre-existing structural decline whilst ensuring landlords maintain the asset’s long-term value.

Vicarious Liability and Design Responsibility

When a failure is traced back to a fundamental error in calculation or material specification, liability may rest with the original architects or structural engineers. This is typically managed through Collateral Warranties, which create a direct contractual link between the professional team and the property owner or tenant. It’s vital to recognise that subsequent structural modifications, if performed without rigorous engineering oversight, can void these original warranties. If an asset’s load-bearing capacity is altered or if proprietary systems are installed incorrectly, the chain of vicarious liability is broken. This leaves the current owner solely responsible for any subsequent failure, reinforcing the need for expert-led design features and validated strengthening interventions.

Common Triggers for Structural Failure and Non-Insured Risks

Most commercial insurance policies are predicated on the occurrence of sudden, accidental events, such as fire or impact. They rarely provide indemnity for issues arising from inherent vice or the gradual decline of material performance. Consequently, the financial liability for structural failure in commercial property often falls entirely on the asset owner when the root cause is identified as a failure to mitigate predictable environmental degradation. The 2025 Charterfields report, which indicated that 88% of surveyed sites were underinsured for building cover, underscores the peril of assuming that standard policies will absorb the costs of structural remediation. When a building is declared unsafe or “unoccupiable” due to instability, the resulting loss of rental income and potential breach of tenant contracts can far exceed the physical cost of the engineering intervention.

In the UK, the “unforeseeable” versus “inevitable” debate is a central pillar of structural damage claims. Insurers argue that whilst a collapse from a freak weather event is unforeseeable, the slow decay caused by sulphate attack or carbonation is an inevitability of time and poor maintenance. This distinction is critical for asset managers. If structural integrity is compromised by deferred maintenance, the liability is typically non-transferable. Engaging in regular Structural Surveys and Testing ensures that these hidden risks are identified before they escalate into non-insured failures, allowing for planned interventions rather than reactive crisis management.

Concrete Carbonation and Reinforcement Corrosion

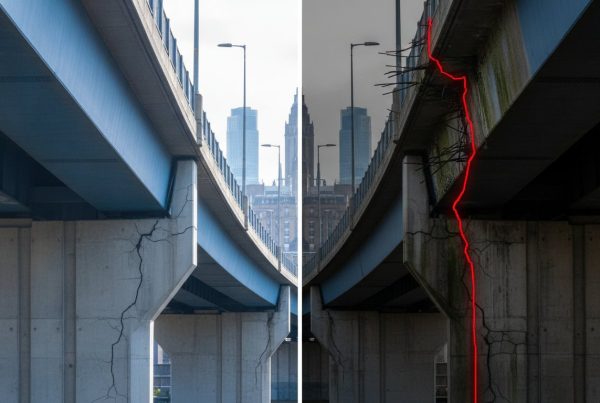

Reinforced concrete assets are particularly susceptible to carbonation, a chemical process where atmospheric carbon dioxide penetrates the substrate and reduces its alkalinity. Once the pH level drops below approximately 9, the passive protective layer around the internal steel reinforcement is destroyed, initiating active corrosion. This oxidation causes the steel to expand, exerting internal tensile pressures that fracture the surrounding concrete from within. Because this process remains invisible until surface cracking appears, it represents a significant hidden liability. Modern detection methods, including half-cell potential mapping and chloride ion analysis, are required to quantify the risk before the load-bearing capacity of the element is fundamentally compromised.

Thermal Movement and Structural Spalling

Large-scale commercial structures must also contend with the physics of thermal movement. The constant expansion and contraction of large spans can lead to significant stress at joints and supports, eventually resulting in structural spalling. When concrete fragments detach from the building envelope, they present an immediate public liability risk that necessitates the urgent installation of exclusion zones. It’s a common error to treat spalling as a cosmetic defect. Masking these areas with standard mortars without addressing the underlying reinforcement corrosion only serves to hide the defect; this behaviour can void original warranties and increase the long-term liability for structural failure in commercial property.

The Building Safety Act 2022 and Evolving Regulatory Liabilities

The introduction of the Building Safety Act 2022 has fundamentally transformed the legal landscape for asset controllers, shifting the focus from voluntary risk management to stringent statutory obligation. One of the most significant changes is the retrospective extension of limitation periods for claims under the Defective Premises Act 1972 to 30 years. This means that liability for structural failure in commercial property can now be pursued for defects in projects completed decades ago, effectively removing the historical safety net of the standard six-year contract limitation. Additionally, the Act establishes Building Liability Orders (BLOs), which permit the High Court to extend liability to associated companies within a corporate group, preventing the use of shell companies to insulate parent organisations from remediation costs.

For higher-risk buildings, the Act mandates the appointment of an “Accountable Person” who bears a statutory duty to assess and manage structural risks. This role is supported by the “golden thread” of information, a digital repository that must contain every detail of a building’s design, construction, and management history. Failure to maintain this record doesn’t just invite regulatory penalties; it significantly diminishes asset valuation. Investors and insurers now view the absence of a verified golden thread as a primary indicator of hidden liability, often resulting in reduced saleability or prohibitive premiums during the due diligence phase of property transactions.

Fostering an organisational culture of transparency is essential for ensuring that the ‘golden thread’ of information remains reliable; to learn more about strengthening your team’s accountability frameworks, check out Core Integrity.

Compliance with Approved Document B and Fire Safety

Structural strengthening interventions must now be viewed through the lens of fire resistance as defined by Approved Document B. Whilst traditional methods might provide the necessary load-bearing enhancement, they often fail to meet the stringent fire safety requirements of the modern regime. This necessitates the use of fire-rated composite systems, such as Tyfo® Fibrwrap® Systems, which are engineered to maintain structural integrity even under high-temperature conditions. Ensuring that structural repairs do not compromise a building’s fire strategy is a critical component of modern liability mitigation, as non-compliant strengthening can lead to the immediate revocation of building assessment certificates.

The Duty to Manage: Proactive vs Reactive Maintenance

The legal distinction between proactive and reactive maintenance is now a central factor in litigation. Courts increasingly apply the “reasonably practicable” standard, questioning whether an asset manager took all necessary steps to identify and rectify structural decline before failure occurred. Ignoring recommendations from Structural Surveys and Testing is frequently viewed as a breach of this duty. By establishing a defensible record of structural care through specialised testing and data-driven monitoring, property owners can demonstrate compliance and significantly reduce their exposure to negligence claims whilst ensuring the long-term safety of the built environment.

Technical Strategies for Liability Mitigation and Asset Life-Extension

Managing the liability for structural failure in commercial property requires a transition from reactive insurance management to proactive engineering intervention. With the Building Cost Information Service (BCIS) forecasting a 15% increase in building costs over the next five years, the economic argument for repair over demolition has never been more compelling. Demolition is no longer the default solution for compromised assets; instead, scientifically validated life-extension strategies allow property owners to preserve the embedded carbon and financial value of their structures. Insurers now prioritise “permanent” remediation over temporary patches, requiring technical evidence that any intervention addresses the root cause of deterioration whilst meeting modern safety standards.

Structural strengthening also plays a pivotal role in the commercial viability of an asset, particularly during a change of use. As retail spaces are repurposed for light industrial or high-density residential use, the existing load-bearing capacity often proves insufficient. By utilising advanced materials, engineers can upgrade the performance of a structure to meet these new operational demands without the need for intrusive and heavy traditional reinforcements. This technical precision is essential for discharging a landlord’s “duty of care,” providing a defensible audit trail that satisfies both regulatory bodies and institutional investors.

CFRP Strengthening and the Tyfo® Fibrwrap® System

Carbon Fibre Reinforced Polymer (CFRP) has emerged as a superior, non-invasive alternative to traditional steel plate bonding or concrete jacketing. Unlike steel, which is heavy and susceptible to its own corrosion cycle, CFRP offers an exceptional strength-to-weight ratio and remains chemically inert. The specific application of Tyfo® Fibrwrap® systems allows for the strengthening of beams, columns, and slabs with minimal impact on the building’s footprint or head height. This is particularly advantageous in active commercial environments where operational downtime must be minimised. These composite systems are engineered to provide confinement and shear enhancement, ensuring that the repaired element exceeds its original design specification.

Structural Surveys and Predictive Testing

Empirical data is the only reliable foundation for a liability mitigation strategy. Comprehensive structural surveys and testing are essential components of the due diligence process, providing a granular understanding of an asset’s current health. Technical assessments typically include:

- Pull-off tests: These measure the bond strength of existing finishes or previous repairs to ensure substrate integrity.

- Carbonation depth analysis: This quantifies the chemical progression of atmospheric CO2 into the concrete, allowing engineers to predict the onset of reinforcement corrosion.

- Chloride ion testing: Essential for identifying salt-induced degradation that can lead to rapid structural decline.

By integrating these findings into a long-term asset management plan, managers can defer major capital expenditure through targeted, incremental repairs. If you are currently assessing a high-value asset with suspected defects, you should consult our engineering team to establish a data-driven remediation programme.

Navigating Remediation with a Specialist Engineering Contractor

The transition from regulatory due diligence to the physical remediation of an asset represents a critical juncture for any property owner. Whilst the legal frameworks previously discussed define the allocation of responsibility, the actual execution of repairs is where the liability for structural failure in commercial property is effectively mitigated. Fragmented procurement, which separates design consultants from the installing contractor, often creates “liability gaps” should an intervention fail to perform as specified. A single point of responsibility, managed by a specialist engineering contractor, ensures that the technical design is perfectly aligned with the site execution, providing a robust defence against future negligence claims.

Managing the stability of a compromised structure during the strengthening phase requires the precise coordination of temporary works. Specialist contractors provide the technical expertise to design and install sophisticated propping and shoring systems that maintain the building’s load-bearing capacity whilst permanent repairs are applied. This end-to-end responsibility encompasses site safety and environmental control, ensuring the remediation process itself doesn’t introduce new structural stressors or public liability risks. This methodical approach is underpinned by significant Professional Indemnity (PI) insurance, providing the long-term security required by institutional investors and their insurers.

Bespoke Design and Feasibility Studies

Generic, “off-the-shelf” repair solutions are often insufficient for the unique stress profiles of complex commercial assets. Effective remediation relies on bespoke engineering calculations, frequently utilising Finite Element Analysis (FEA) to simulate how composite reinforcements will interact with the existing substrate under various load cases. Collaborating with specialist engineering contractors during the feasibility stage allows for the development of tailored programmes that are both technically viable and economically efficient, ensuring that the proposed strengthening satisfies modern building assessment requirements.

Professional Indemnity and Design Responsibility

Composites Construction UK assumes the primary design risk for structural strengthening projects, providing a seamless transfer of liability from the asset owner to the specialist contractor. This is a vital distinction; by appointing a partner that manages both design and installation, property owners eliminate the potential for disputes between third-party engineers and site teams. This reliability is further reinforced by the use of proprietary systems and certified installers, ensuring every repair meets the rigorous standards required by the Building Safety Regulator. Before commissioning works, asset managers should verify:

- The contractor’s ability to provide project-specific PI insurance for both design and build.

- The presence of validated empirical data for all proposed material systems.

- A clear methodology for the management of temporary works and structural monitoring.

To discuss your asset’s structural integrity and develop a defensible remediation strategy, contact our engineering team today.

Securing the Future of Commercial Infrastructure

The evolution of the UK’s building safety regime represents a permanent shift from administrative risk allocation to technical accountability. As explored throughout this guide, the liability for structural failure in commercial property is no longer a historical risk that can be ignored, but an active financial exposure that demands empirical management. By moving beyond the limitations of standard insurance and embracing the digital “golden thread” of information, asset managers can transform their portfolios from potential liabilities into resilient, long-term investments that satisfy the most stringent regulatory scrutiny.

Composites Construction UK serves as the exclusive UK licensee for Tyfo® Fibrwrap® systems, providing the specialised design and installation expertise required for the world’s most critical infrastructure. With decades of history in structural life-extension, our engineers provide the validated data and professional indemnity needed to discharge your statutory duties with absolute confidence. Please consult our specialist engineers on structural risk mitigation to secure your asset’s structural integrity for the future. Proactive engineering remains the only certain path to ensuring both public safety and sustained commercial value.

Frequently Asked Questions

Who is responsible for structural repairs in a commercial lease?

Responsibility is typically dictated by the specific covenants within the lease agreement. Under a Full Repairing and Insuring (FRI) lease, the burden of maintaining the structural envelope and core elements usually rests with the tenant. Conversely, in multi-let assets, the landlord often retains responsibility for the primary structure, recovering costs through a service charge. It’s essential to review the “red line” plans to define the exact boundaries of repair obligations.

Does commercial building insurance cover structural failure?

Standard commercial policies generally exclude structural failure resulting from gradual deterioration, wear and tear, or inherent vice. Coverage is typically restricted to sudden, accidental damage caused by specified perils such as fire, flood, or impact. Consequently, failures arising from deferred maintenance or progressive chemical processes like carbonation are often classified as non-insured risks, leaving the asset owner financially responsible for remediation.

What is the “Accountable Person” under the Building Safety Act 2022?

The Accountable Person is an individual or organisation that owns or has a legal obligation to repair the common parts or structure of a higher-risk building. This role carries a statutory duty to assess and manage risks related to fire and structural safety. For buildings exceeding 18 metres or seven storeys, the Accountable Person must demonstrate that all “reasonably practicable” steps have been taken to prevent failure.

How long is a developer liable for structural defects in the UK?

Following the enactment of the Building Safety Act 2022, the limitation period for claims under the Defective Premises Act 1972 has been extended to 30 years for retrospective projects. For new builds completed after June 2022, the period is 15 years. This significantly broadens the window during which developers and contractors can be held legally responsible for latent flaws that compromise the liability for structural failure in commercial property.

Can a tenant stop paying rent if the building is structurally unsound?

Tenants generally possess no automatic legal right to withhold rent due to structural instability unless the lease contains a specific rent cesser clause. Most such clauses are only triggered when damage is caused by an insured peril that renders the premises unoccupiable. Unilaterally stopping rent payments often results in a breach of contract and potential forfeiture, regardless of the building’s physical condition or perceived safety risks.

What are the first signs of structural failure in a commercial property?

Initial indicators often include the manifestation of longitudinal cracks in reinforced concrete, significant floor deflection, or the presence of rust staining on external masonry. Visible spalling, where concrete fragments detach from the substrate, is a critical sign of advanced reinforcement corrosion. These symptoms necessitate immediate structural surveys to quantify the extent of the underlying deterioration before the load-bearing capacity is fundamentally compromised.

How does CFRP strengthening mitigate structural liability?

Carbon Fibre Reinforced Polymer (CFRP) strengthening mitigates liability for structural failure in commercial property by providing a permanent, non-corrosive solution that restores or enhances load-bearing capacity. These systems allow for quantifiable performance improvements that satisfy insurer requirements for high-integrity repairs. By addressing the root cause of instability without the weight of traditional steel, the functional lifespan of the asset is secured with minimal operational downtime.

What is the difference between a latent defect and a patent defect?

A patent defect is a flaw that is readily observable upon a reasonable inspection, such as visible masonry cracking or water ingress. In contrast, a latent defect is an inherent flaw in design or construction that remains concealed within the structure for an extended period, such as insufficient reinforcement cover. Liability often hinges on identifying latent defects that were present but undiscovered at the time of purchase or lease commencement.